- Part I: Information on the Like-Kind Exchange

- Part II: Related Party Exchange Information

- Part III: Realized Gain or Loss, Recognized Gain, and Basis of Like-Kind Property Received

- Part IV: Deferral of Gain From Section 1043 Conflict-Of-Interest Sales

How do I complete IRS Form 8824?

There are four parts to this two-page tax form:

- Part I: Information on the Like-Kind Exchange

- Part II: Related Party Exchange Information

- Part III: Realized Gain or Loss, Recognized Gain, and Basis of Like-Kind Property Received

- Part IV: Deferral of Gain from Section 1043 Conflict-of-Interest Sales

We’ll go through each of these parts, one step at a time. Let’s begin with line-by-line instructions for Part I.

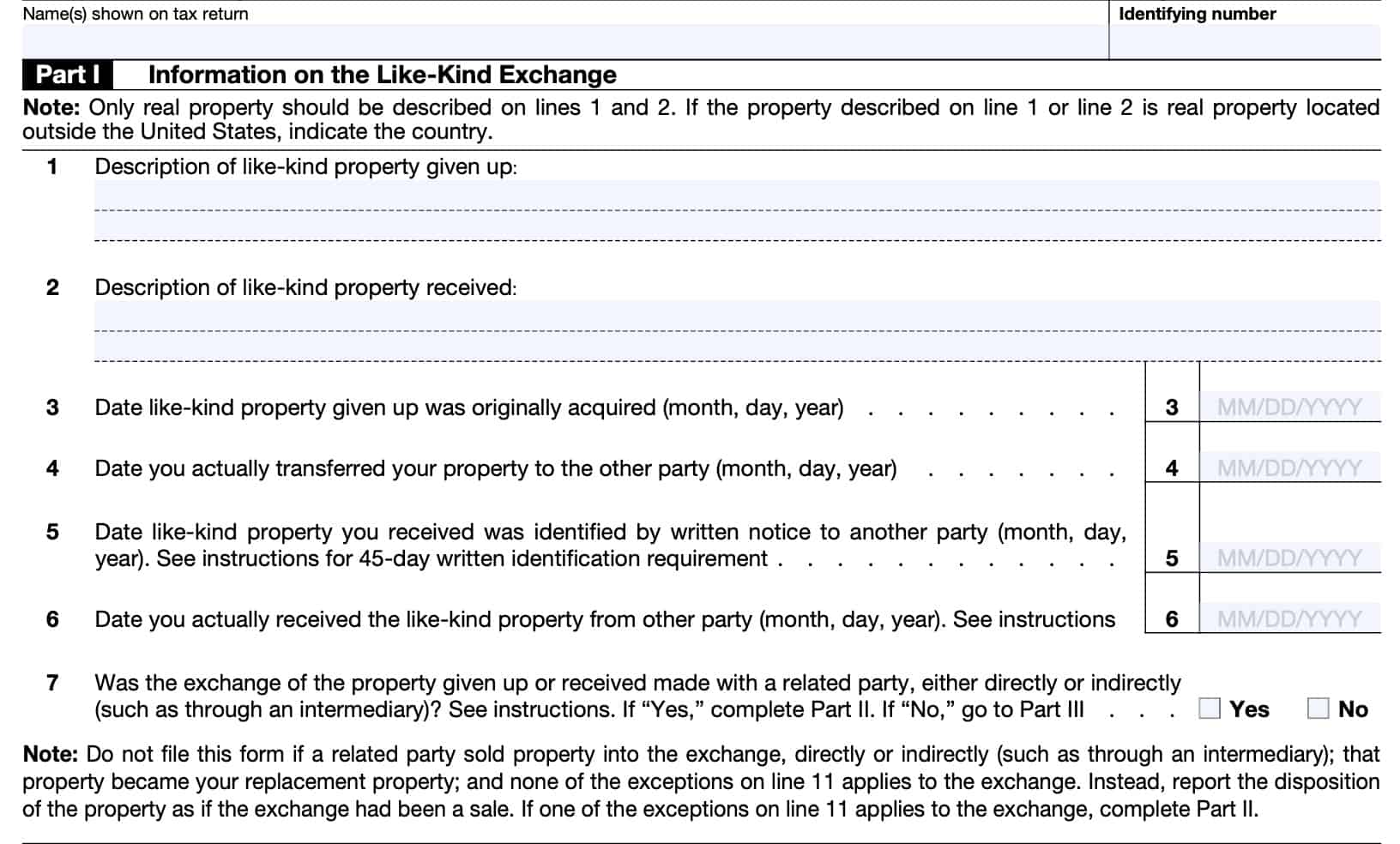

Part I: Information on the Like-Kind Exchange

Part I should contain information on the like-kind exchange.

Line 1: Description of like-kind property given up

As a general rule, only real property should be described on Lines 1 and 2. This includes intangible property that is treated as real property for like-kind exchange purposes.

In Line 1, enter the address and type of property given up. If the property does not have an address, enter a short description. If the property is outside the United States, list the country where the property is.

Line 2: Description of like-kind property received

In Line 2, enter the address and type of property that you received in this exchange.

As with Line 1, if the property does not have an address, enter a short description. If the property is outside the United States, list the country where the property is.

Line 3: Date like-kind property given up was originally acquired

Enter the date that you originally acquired the relinquished property.

Line 4: Date you actually transferred your property to the other party

Enter the date that you actually transferred ownership of your property to the other party.

Line 5: Date like-kind property you received was identified by written notice

On Line 5, enter the date of the written identification of the like-kind property you received in a deferred exchange.

To comply with the 45-day written identification requirement, the following conditions must be met.

- The like-kind property you receive in a deferred exchange is designated in writing as replacement property either

- In a document you signed or

- In a written agreement signed by all parties to the exchange

- Real property should be described using a legal description, street address, or distinguishable name

- You fax, hand deliver, mail, or otherwise send the document you signed to:

- The person required to transfer the replacement property to you (including a disqualified person), or

- To another person involved in the exchange (other than a disqualified person); or

Generally, a disqualified person is either your real estate agent at the time of the transaction or a person related to you. For more details, see Treasury Regulations Section 1.1031(k)-1(k). Also, see details on disqualified persons in IRS Publication 544, Sales and Other Dispositions of Assets.

If you received the replacement property before the end of the 45-day period, you are automatically treated as having met the 45-day written identification requirement. In this situation, enter the date that you received the new property.

Line 6: Date you actually received the like-kind property from other party

Enter the date that you actually received the like-kind property from the other party.

According to the 180-day exchange period rule, you must have received the replacement property by the earlier of the following dates:

- The 180th day after the date you transferred the property given up in the exchange

- The due date of your tax return for the year in which you transferred the property given up, including extensions

Line 7: Was exchange of property given up or received made with related party?

Answer this question, ‘Yes/No.’

If the answer is ‘Yes,’ go to Part II. If the answer is ‘No,’ skip Part II and go directly to Part III.

Related party

According to IRC Section 1031(f), special rules apply to exchange transactions between related parties, either directly or indirectly.

A related party may be one of the following:

- Spouse

- Child

- Grandchild

- Parent or grandparent

- Brother & sister

- Related entity, such as S-corporation, partnership, trust, estate, or tax-exempt organization

Examples of indirect exchange transactions with a related party include:

- An exchange made with a related party through a qualified intermediary (QI) or exchange accommodation titleholder (EAT), as defined in IRS Publication 544; or

- An exchange made by a disregarded entity if you or a related party owned that entity

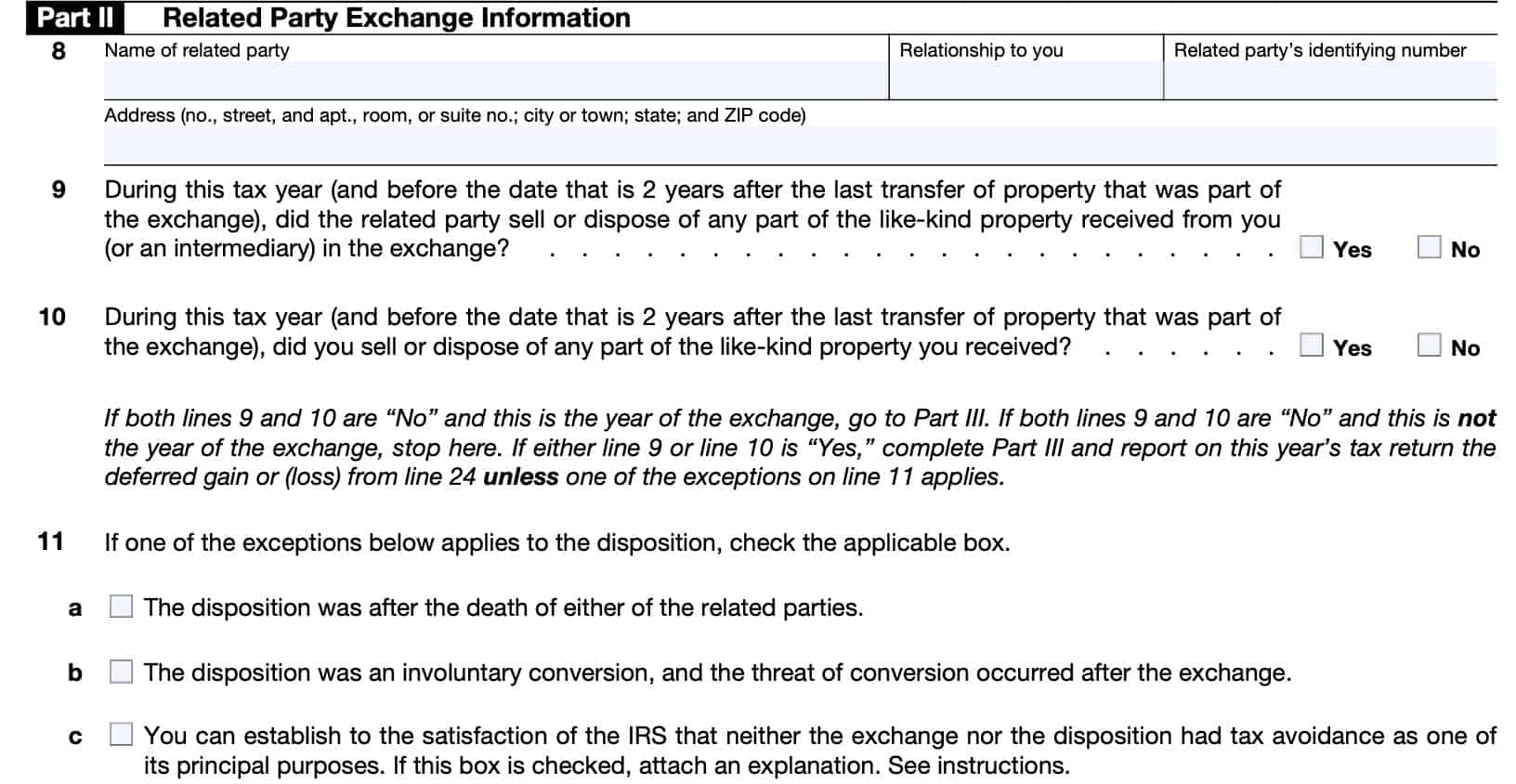

Part II: Related Party Exchange Information

In Part II, you’ll enter the required information regarding your exchange with a related party.

Line 8

In Line 8, enter the following information for the related party:

- Related party’s name

- Relationship to taxpayer

- Related party’s identifying number

- Address

Line 9

Did the related party sell or dispose of any part of the like-kind property received from you, or an intermediary in the exchange:

- During the current tax year, and

- Before the 2 year anniversary after the last transfer of property that was part of the exchange

If true, answer ‘Yes.’ Otherwise, answer ‘No.’

Line 10

Did you sell or dispose of any part of the like-kind property that you received as part of the exchange process:

- During this tax year, and

- Before the 2-year anniversary of the last property transfer

If so, answer ‘Yes.’ Otherwise, answer ‘No.’

If both Line 9 & Line 10 contain ‘No’ and this is the year of the exchange, go to Part III. Stop here if both Lines are ‘No’ and this is not the year of the exchange.

If either line is ‘Yes,’ complete Part III and report the deferred gain or loss from Line 24 below, unless one of the exceptions from Line 11 applies.

Line 11: Exceptions

There are several possible exceptions to the related party exchange rules. If one of these exceptions applies to your situation, check the appropriate box:

- The disposition was after the death of either related party

- Disposition was an involuntary conversion, and the threat of conversion happened after the exchange took place

- You can establish to the IRS’ satisfaction that tax avoidance was not the principal purpose for either the exchange or the disposition.

- Attach a written explanation to the completed Form 8824

In general, the IRS will not consider tax avoidance as the principal purpose in the following situations:

- Disposition of property in a nonrecognition transaction

- Like-kind exchange where neither party receives a tax advantage from shifting asset basis between the exchanged properties

- Exchange of undivided interests in different properties resulting in each party holding either:

- The entire interest in a single property, or

- Larger undivided interest in either property

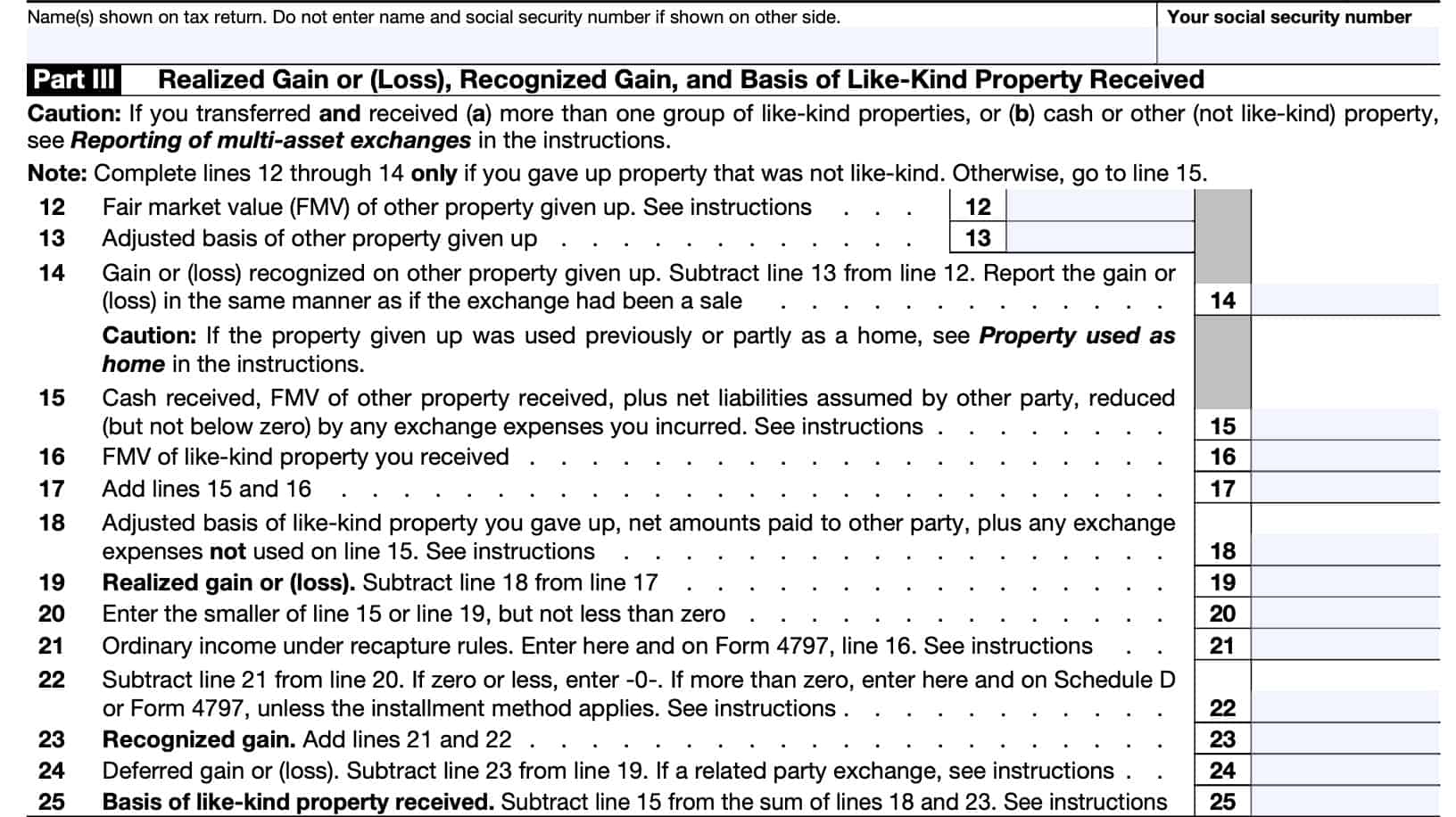

Part III: Realized Gain or Loss, Recognized Gain, and Basis of Like-Kind Property Received

In Part III, we’ll calculate any realized gain or loss, recognized gain, and basis of property received in the like-kind exchange transaction.

If you gave up property that was not like-kind, complete Lines 12 through 14. Otherwise, go directly to Line 15, below.

Line 12: FMV of other property given up

Enter the fair market value (FMV) of the other property that you gave up during the exchange. Only complete this line if other property that doesn’t qualify as like-kind property was part of the exchange, in addition to the like-kind property.

Line 13: Adjusted basis of other property given up

Enter the adjusted basis of the other property.

Line 14: Gain or loss on other property given up

Subtract Line 13 from Line 12.

This represents the recognized gain or loss on the other property. Report this gain or loss as if the exchange had been a property sale.

If the property that you gave up was previously used as a primary residence, you may be able to exclude part or all of the gain from taxable income.

Line 15

Include the sum of the following:

- Amount of cash received in the transaction

- FMV of other property received

- Net liabilities assumed by the other party

- Reduced by exchange expenses you may have incurred during the transaction

Net liabilities include remaining liabilities the other party may have incurred, after subtracting:

- Total liabilities you incurred as part of the transaction

- Cash that you paid the other party

- FMV of non like-kind property you gave up as part of the transaction

The result is also known as boot. Boot is the portion of the sales proceeds you receive from a 1031 exchange that isn’t re-invested in a replacement property. Boot may be subject to taxation in the tax year of the completed exchange.

Line 16: FMV of like-kind property received

Enter the fair value of like-kind property you received as a result of this transaction.

Line 17

Add Line 15 and Line 16. Enter the total here.

Line 18

In Line 18, enter the sum of the following:

- Adjusted basis of like-kind real property that you gave up during the transaction

- Exchange expenses, if applicable

- Do not include expenses used to reduce the amount that you reported on Line 15, above

Line 19: Realized gain or loss

Subtract Line 18 from Line 17, above. This is your realized gain or loss.

Line 20

Enter the smaller of:

Do not enter a number less than zero.

Line 21: Ordinary income under recapture rules

If you disposed of section 1245, 1250, 1252, 1254, or 1255 property, you may be required to recapture part or all of the realized gain in Line 19 as ordinary income.

Figure the amount to enter on Line 21 as follows.

Section 1245 real property

For Section 1245 property, enter the smaller of the following:

- Total adjustments for deductions allowed or allowable to you or any other person for depreciation or amortization

- Up to the amount of gain shown on Line 19; or

Deductions allowed are tax deductions actually taken on your annual tax return.

Deductions allowable are total tax deductions you are allowed to take, whether or not you actually took them.

Section 1250 property

If reporting Section 1250 property, enter the smaller of:

- Gain you would have had to report as ordinary income because of additional depreciation if you had sold the property, or

- Refer to Line 26 instructions for IRS Form 4797

- Gain shown on Line 20, above, or

- Excess, if any, of the gain outlined above, over the FMV of Section 1250 property received

Section 1252, 1254, and 1255 property

The rules for these types of property are similar to the rules for Section 1245 property.

See Regulations Sections 1.1252-2(d) and 1.1254-2(d) and Temporary Regulations section 16A.1255-2(c) for details.

If the installment sales method applies to this exchange:

- See IRC Section 453(f)(6) to determine the installment sale income taxable for this year and report it on IRS Form 6252;

- Enter on IRS Form 6252, line 25 or 36, the Section 1252, 1254, or 1255 recapture amount you figured on Line 21

- Don’t enter more than the amount shown on Form 6252, Line 24 or 35;

Line 22

Unless the installment sales method applies, you may need to report gains on Form 4797 or Schedule D of your tax return.

- Report gains from the exchange of property used in a trade or business (and other noncapital assets) on IRS Form 4797

- Report capital gains from the exchange of capital assets on Schedule D of your income tax return

Line 23: Recognized gain

Add lines 21 & 22. This is your recognized gain on the transaction.

Line 24: Deferred gain (or loss)

If Line 19 is a loss, enter it on Line 24. Otherwise, subtract the amount on Line 23 from the amount on Line 19 and enter the result.

Line 25: Basis of like-kind property received

Add Line 18 and Line 23. Subtract Line 15 from the result. This is the basis of like-kind property received in the exchange.

Your basis in other property (not like-kind) received in the exchange, if any, is its FMV.

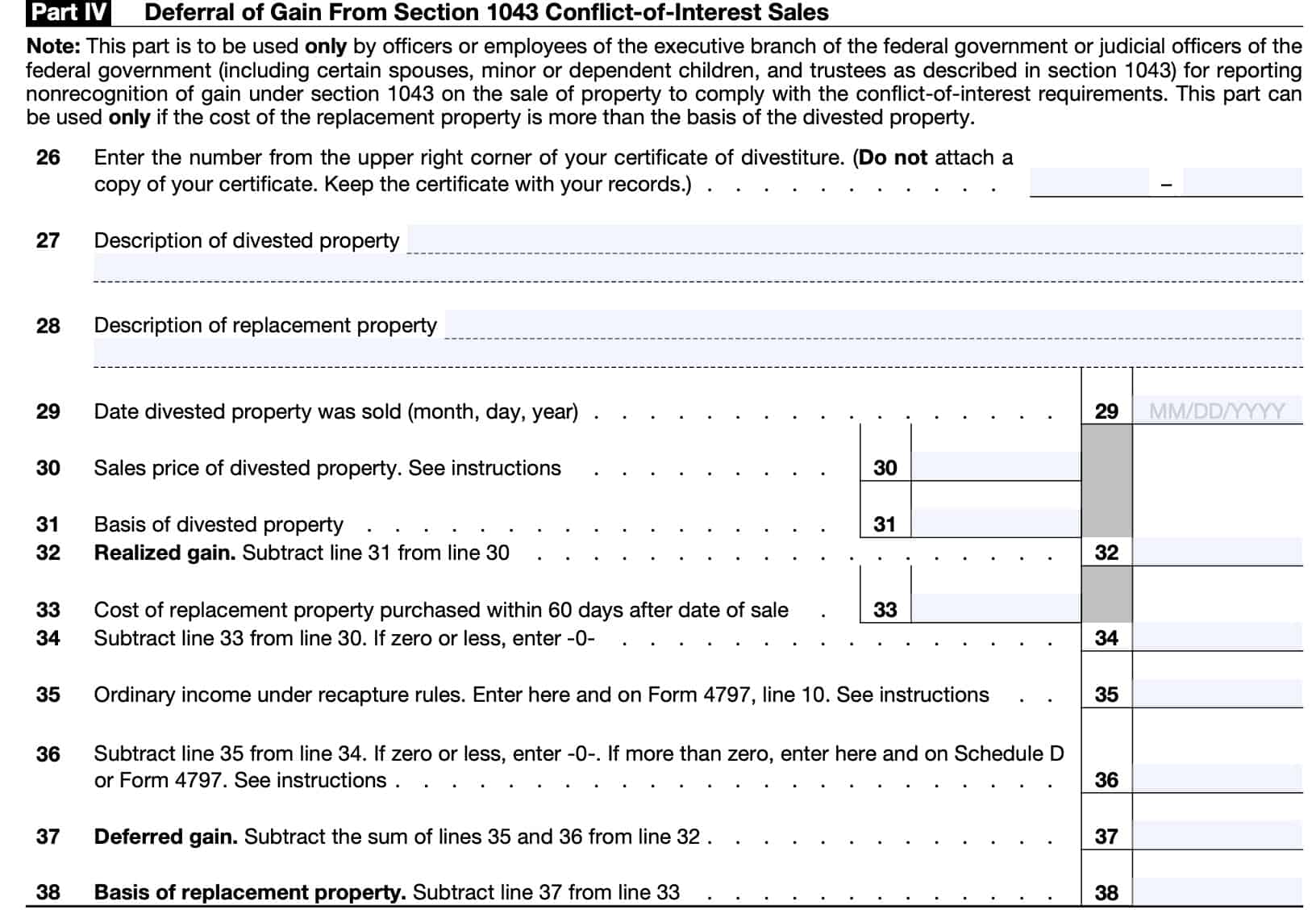

Part IV: Deferral of Gain From Section 1043 Conflict-Of-Interest Sales

Certain members of the executive branch of the federal government and judicial officers of the federal government use Part IV to elect to defer gain on conflict-of-interest sales. See the IRS Form 8824 Instructions for more specific guidance on which judicial officers must complete Part IV.

Use Part IV to report nonrecognition of gain under Section 1043, only if the replacement property cost is more than the basis of the divested property.

Line 26

Enter the number from the upper right corner of your certificate of divestiture. Keep your certificate with your tax records.

Line 27: Description of divested property

Enter a plain description of the property that you relinquished.

Line 28: Description of replacement property

Enter a plain description of the property that you received.

Line 29: Date divested property was sold

Enter the date of the sales transaction for the divested property.

Line 30: Sales price of divested property

Enter the sales property that you sold, after subtracting transaction costs, such as real estate broker fees.

Line 31: Basis of divested property

Enter the adjusted tax basis for the divested property.

Line 32: Realized gain

Subtract Line 31 from Line 30. This your realized gain.

Line 33: Replacement property cost

Generally, to defer capital gains, the acquisition of the replacement property must take place within 60 days of the sale of the property you are relinquishing.

Enter the cost of the property that you purchased within 60 days of the sale of the other property.

Line 34

Subtract Line 33 from Line 30. If this results in a negative number, enter ‘0.’

Line 35: Ordinary income under recapture rules

To arrive at this result, do the following:

- Use IRS Form 4797, Part III to figure ordinary income under recapture rules

- Enter the amount from Form 4797, Line 31

- Enter this number on Form 4797, Line 10, Column (g). In Column (a), enter ‘From IRS Form 8824, Line 35). Leave columns (b) through (f) blank.

Line 36: Capital gain

Subtract Line 35 from Line 34. If zero or less, enter ‘0.’

If the result is a positive number, enter the result here and on one of the following:

- If you sold a capital asset:Schedule D, Line 36

- If you sold property used in a trade or business: IRS form 4797, Line 2 (long-term) or Line 10 (short-term)

- If you held a qualified investment in a qualified opportunity fund (QOF): IRS form 8997

Line 37: Deferred gain

Add Line 35 and Line 36. Subtract this sum from Line 32. This is the deferred gain.

Line 38: Basis of replacement property

Subtract Line 37 from Line 33. This is the new tax basis for the replacement property for tax reporting purposes.

Video walkthrough

Watch this instructional video to learn more about reporting like-kind exchanges on IRS Form 8824.

Frequently asked questions

What is a related party?According to the Internal Revenue Service, a related party includes your spouse, child, grandchild, parent, grandparent, brother, sister, or a related corporation, S corporation, partnership, trust, estate, or tax-exempt organization.

Where can I find IRS Form 8824?

You can find this tax form on the IRS website. For your convenience, we’ve attached the latest version of IRS Form 8824 to this article.